The current watch market in 2026 presents a peculiar opportunity: while established brands’ pricing remains elevated and allocation scarcity persists for the Holy Trinity and Rolex sports models, independent watchmakers offer increasingly compelling value propositions that serious collectors systematically overlook.

The prejudice against independents stems from outdated assumptions that production scale equates to legitimacy, brand recognition determines quality, and resale liquidity justifies premium pricing. These beliefs might have held merit twenty years ago. Today, they represent blind spots, creating genuine opportunities for collectors who prioritize horological substance over brand cachet. That’s exactly why brands like Greubel Forsey, F.P. Journe, Philippe Dufour, De Bethune, and Akrivia are at an all-time high.

The economic argument for independents begins with production limitations that established manufactures cannot replicate. For instance, De Bethune produces approximately 200 watches annually. Grönefeld produces fewer than 100. Ferdinand Berthoud, backed by Chopard, maintains production below 50 pieces across all references. These aren't artificial scarcity strategies—they reflect genuine manufacturing constraints where every component receives individual attention impossible at the large manufacture scale.

When Patek Philippe produces around 60,000 watches annually, and Audemars Piguet exceeds 50,000, the math is straightforward: independent production represents genuinely limited availability rather than marketing theater. Collectors who dismiss independents as ‘too small’ or not well established enough, miss the fundamental point that scarcity without substance remains worthless, but substance with genuine scarcity creates long-term value. Consider recent auction results for F.P. Journe and other independents.

The creative freedom independents demonstrate consistently exceeds manufacture capabilities constrained by shareholder expectations, heritage preservation, and market research committees. Block RG's geometric case architecture—featuring knife-edge angles and surfaces that challenge traditional finishing techniques—exists because founder Romas Gimbutis possesses both technical capability and creative autonomy. No manufacture risk committee would approve such radical departures from established aesthetics.

Greubel Forsey presents complications within deliberately unconventional case proportions that prioritize wearability over market research data about optimal case diameters. Just look at the GMT Sport, which is all about ergonomics. These approaches don't emerge from manufactures burdened by quarterly sales targets and brand consistency requirements. Independent watchmakers create what they believe represents horological excellence rather than what focus groups indicate will sell.

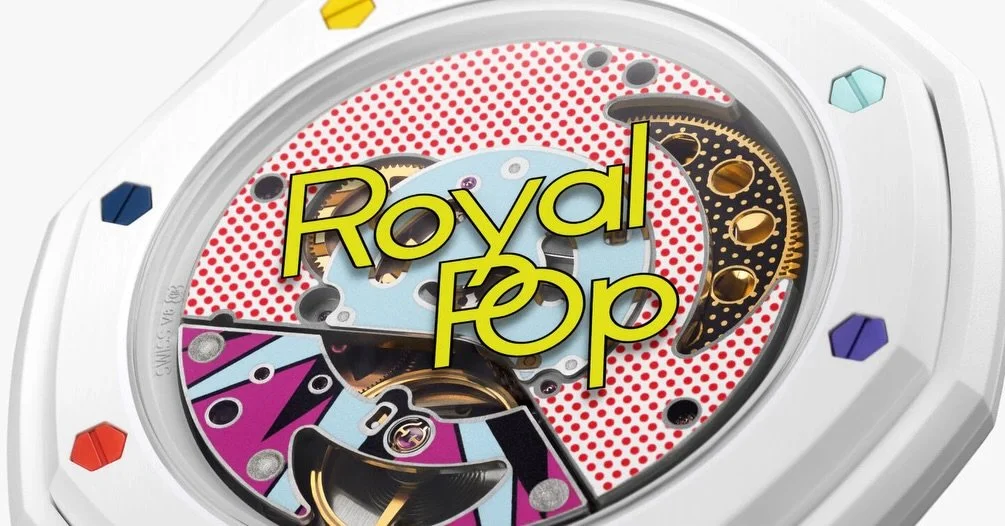

The finishing standards independents achieve often surpass manufacture execution despite—or perhaps because of—smaller production volumes. CVSTOS's visible architecture through their sapphire crystal cases showcases exceptional finishing, anglage, and hand-polished bevels across components that many manufactures would hide beneath solid case backs. The transparency serves two purposes: demonstrating finishing quality and making the mechanical operation visible.

Watch collectors who've examined both the manufacture and independent finishing frequently report that independents match or exceed Holy Trinity standards at a fraction of the price. This isn't universal—some independents prioritize innovation over finishing perfection—but the best independent work rivals that of established names. The market hasn't recognized this reality through pricing, creating valuation disconnects favoring collectors who actually examine watches rather than relying on brand reputation. For instance, take a look at the latest releases from Armin Strom, like the Resonance GMT Manufacture Edition—a 50-piece limited edition. A young manufacture that produces fewer than 500 watches a year.

The secondary market argument against independents—poor liquidity and low value retention—deserves examination rather than reflexive acceptance. Yes, independents face narrower collector bases than Patek Philippe or Audemars Piguet. Yes, finding buyers requires more effort than selling mainstream references. But this market inefficiency works both ways.

Buying independents at 30-40% discounts to retail because sellers struggle to find buyers creates acquisition opportunities unavailable with allocated manufacture pieces trading above retail. For collectors building personal collections rather than investment portfolios, liquidity concerns matter less than acquisition value. If you're wearing the watch rather than flipping it, narrow secondary markets represent buying advantages rather than exit problems.

De Bethune and MB&F represent the pinnacle of independent watchmaking innovation, combining proprietary balance-wheel technology and a distinctive aesthetic identity. The MB&F LM Sequential Flyback showcases what independent watchmaking delivers compared with established manufacture alternatives at similar prices. Ferdinand Berthoud offers classical haute horlogerie executed with Chopard manufacturing support—independence with manufacture infrastructure backing. Grönefeld Brothers appeal to collectors who appreciate understated elegance and hand-finished movements, with every surface receiving traditional artisanal attention, and so exquisitely finished that they could be worn on their movement side.

The trajectory favors independents as collecting demographics shift toward enthusiasts who research beyond brand names. Younger collectors educated through online communities and direct access to watchmakers increasingly prioritize technical merit over heritage storytelling. This demographic transition creates tailwinds for independents who've historically struggled against old manufacture marketing budgets and established distribution networks. Social media enables independents to reach collectors directly, circumventing traditional retail channels where manufacture relationships dominate shelf space. The tools favoring David over Goliath multiply annually. The number of new independent watchmaking brands released in the past three yours has more than doubled.

From a watch-collecting strategy perspective, independents deserve meaningful portfolio allocation—not as speculative plays, but as opportunities to acquire genuine horological achievements at valuations divorced from brand premiums and inflated auction results. The watches exist; the watchmaking quality warrants attention; and the pricing reflects market inefficiency rather than intrinsic value. One of the biggest downsides of buying a watch from an independent brand is limited servicing options: most traditional watchmakers are not qualified to work on these watches, and parts won’t be sold to them directly. Additionally, their proprietary in-house calibres are sometimes unique and difficult to service.

Independent watchmakers create what manufactures cannot: watches uncompromised by market research, production scale requirements, or shareholder expectations. That creative freedom deserves support from collectors who claim to value horological excellence.